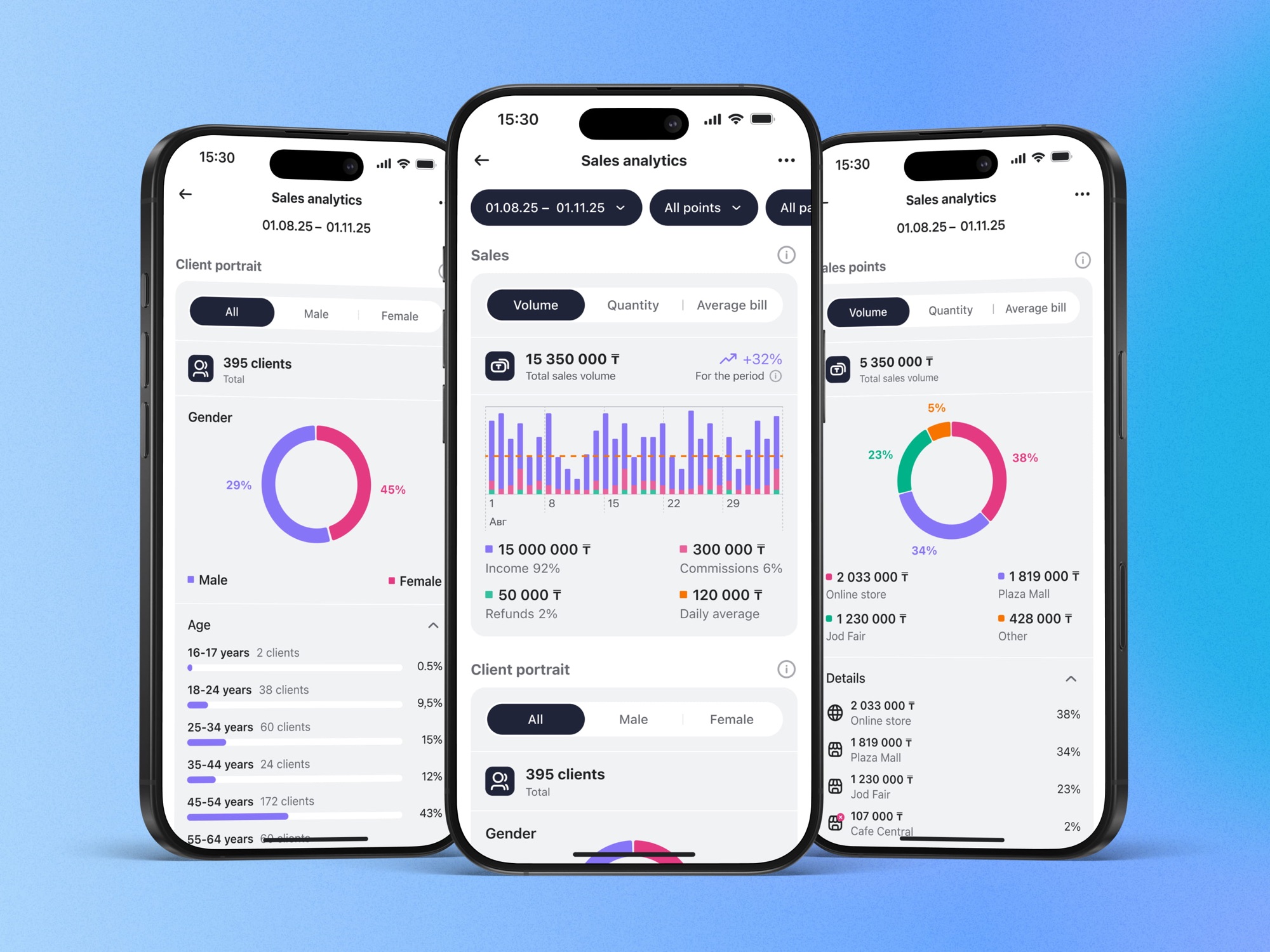

Led product design and discovery for Kazakhstan's flagship SME merchant platform — from MVP to 40,000+ active merchants. Designed and launched Kazakhstan's first interbank Unified QR system, lifting transaction success to 98.5% and merchant satisfaction to a 4.92 sustained VoC.

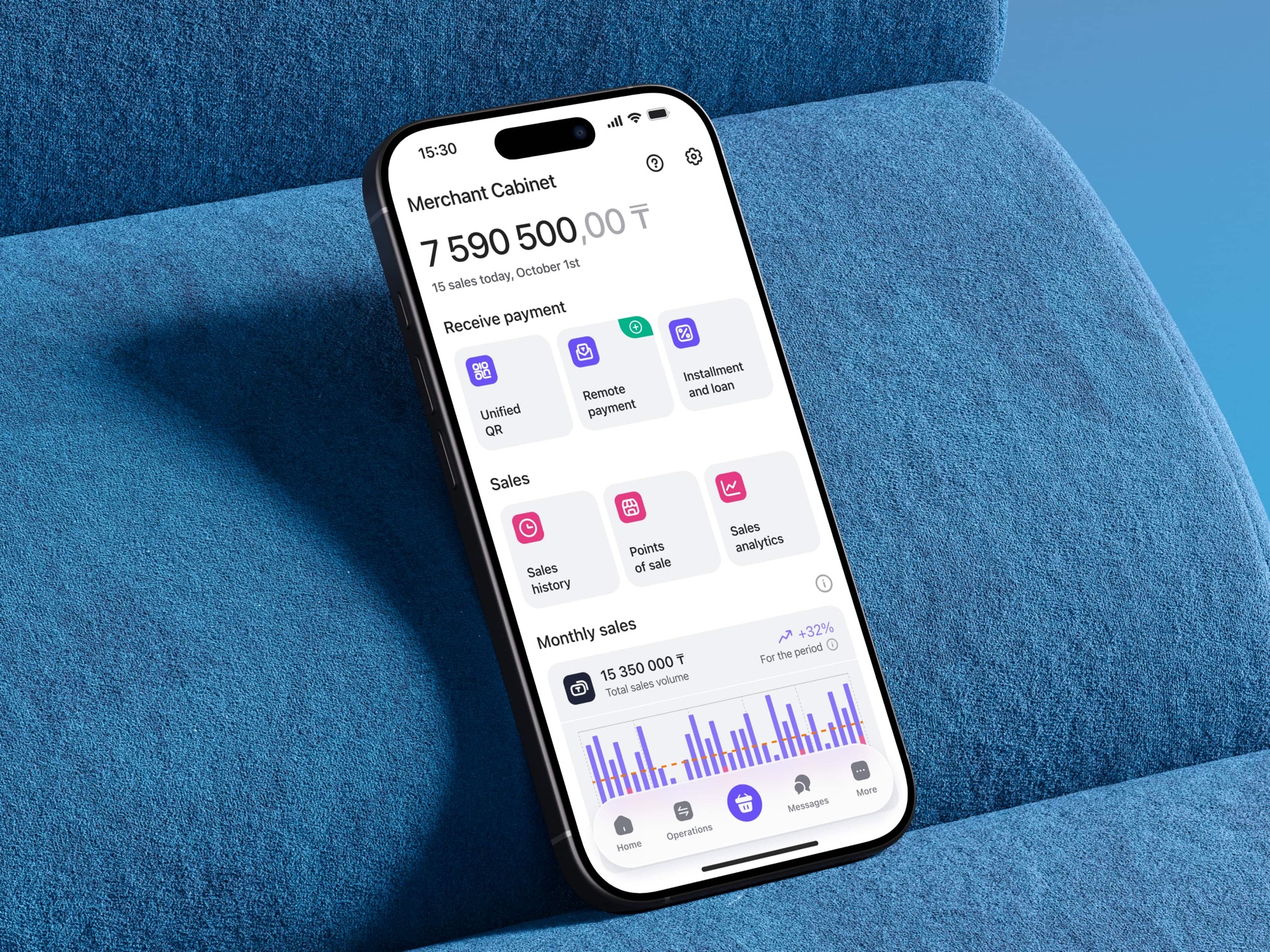

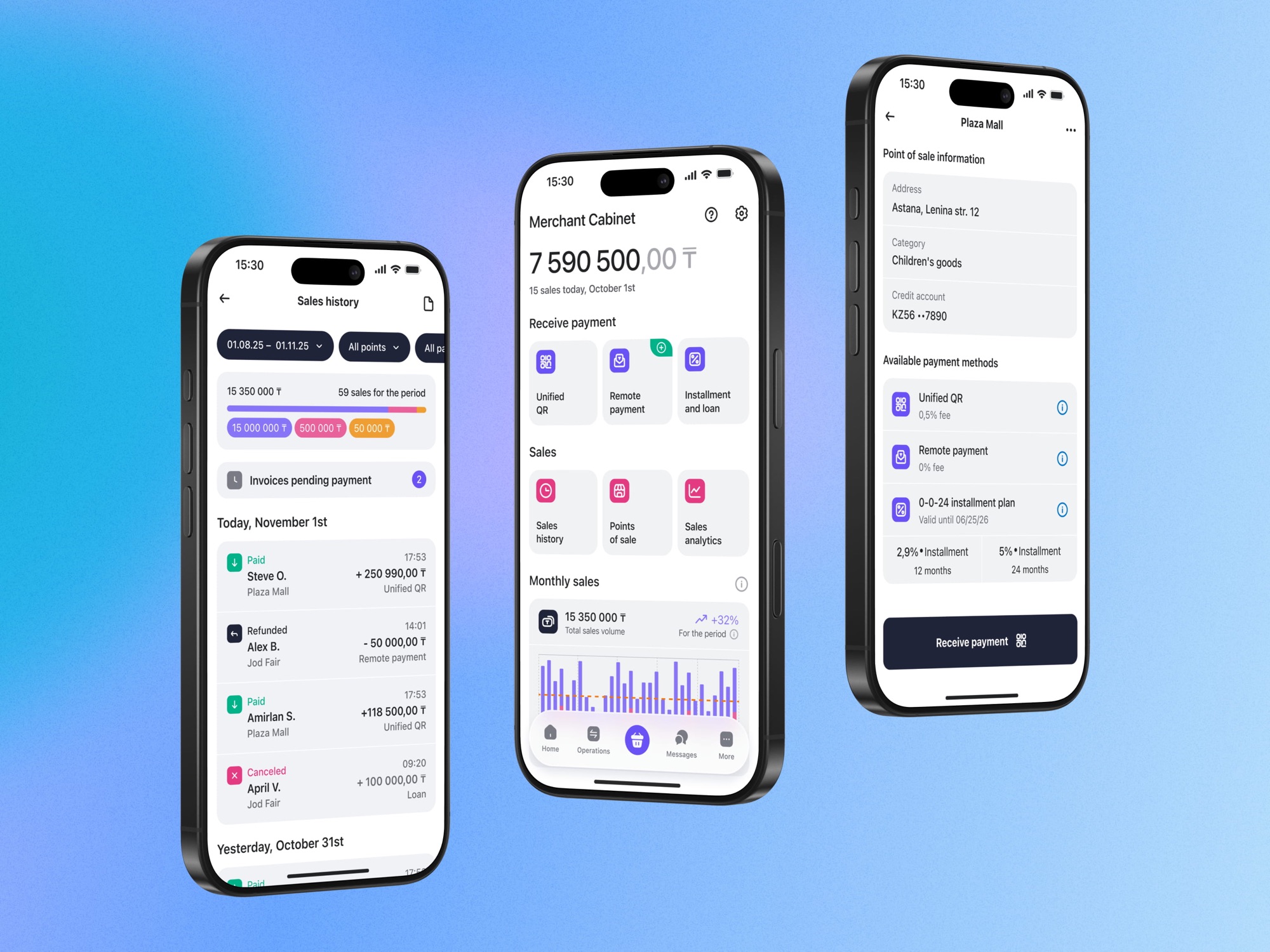

Home Credit Bank Business is the merchant banking platform for small and medium businesses in Kazakhstan — payments, QR acquiring, sales analytics, and business management tools in one place.

I joined as lead product designer at the moment Merchant Cabinet was an MVP with limited features and low perceived value, while the bank was simultaneously preparing for a national-level product milestone: launching Kazakhstan's first interbank Unified QR — a state-driven initiative to unify QR payments across all major banks under a single standard.

Two challenges sat on top of each other. Mature the merchant experience to match enterprise scale. And design a payment flow that hides the complexity of five banks behind a single QR a merchant can generate in under three seconds.

My process is built around closing the loop between hypothesis and shipped metric, not delivering pixel-perfect Figma files. For Merchant Cabinet I ran:

The headline finding of that research wasn't about UI. The #1 pain was multi-bank complexity, and the deepest anxiety was "will the payment actually reach me?" That moved the brief from "improve the merchant UI" to "enable any-bank payments and make settlement trustworthy" — a reframe that changed what we built, not how it looked. We were close to shipping an information architecture based on assumptions from the bank side; the interviews rewrote it.

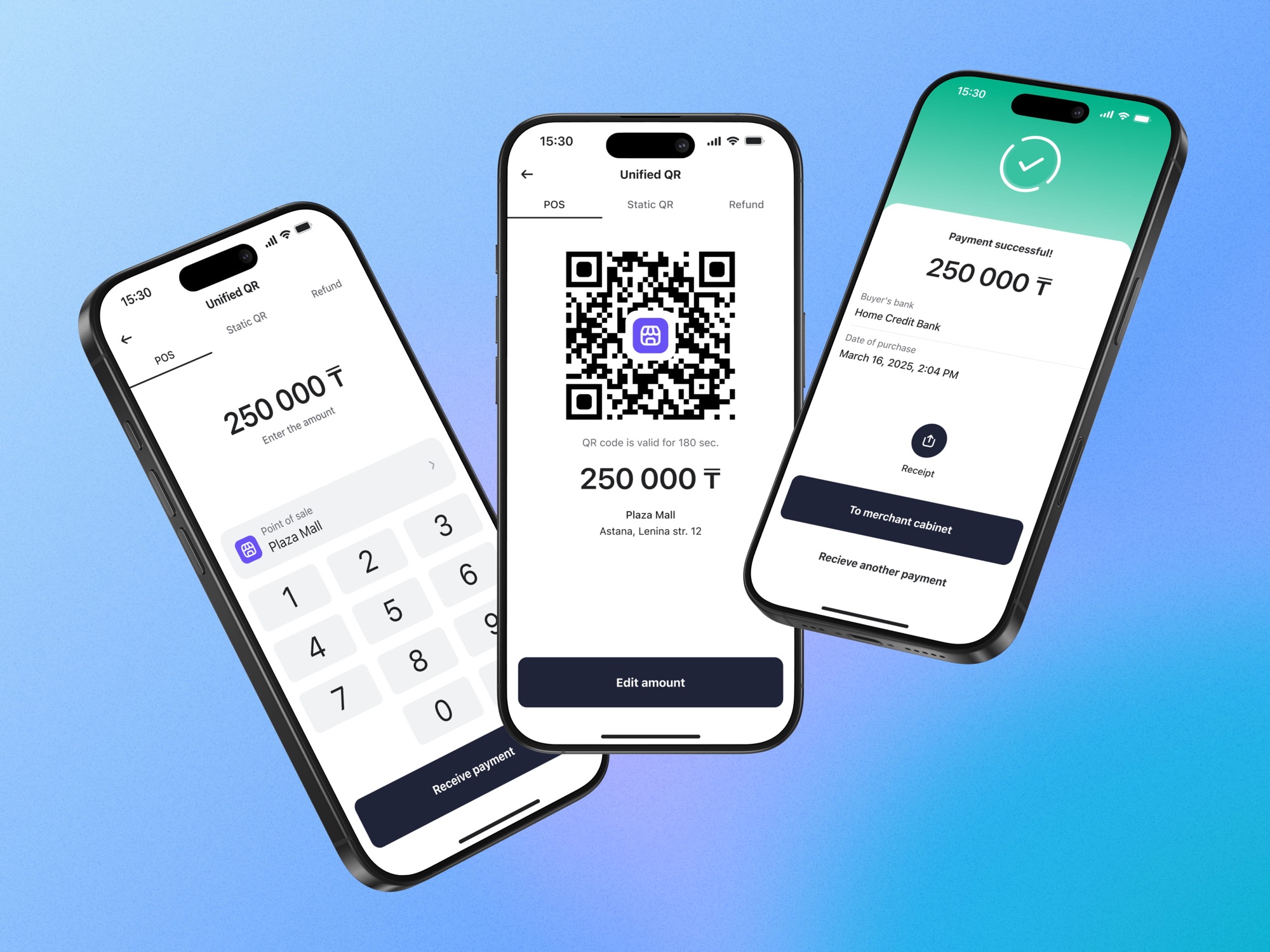

Since trust was the real job, I spent the design budget on confirmation speed and receipt clarity — the merchant sees, fast and unambiguously, that the money landed — and hid the cross-bank complexity behind one code.

Each feature passed through one cycle: research → prototype → test → launch → metrics → iterate. No feature shipped without an explicit hypothesis tied to a measurable outcome.

The Unified QR launch was the most consequential design decision of the project, and it had nothing to do with how the QR looked.

The temptation was to expose the multi-bank architecture in the UI — let merchants choose which bank to receive payment through, show the routing logic, surface the technical reality. That would have been honest, and unusable.

I made the opposite call: the merchant flow shows nothing of the routing complexity. A merchant generates one QR — dynamic for a specific amount, static tied to a POS — and the system handles the inter-bank logic invisibly. Two flows. Three taps to a working QR. The customer scans with any banking app in Kazakhstan, and it works.

This was less a design task than a product-strategy call: which complexity stays in the system, and which leaks into the merchant's day.

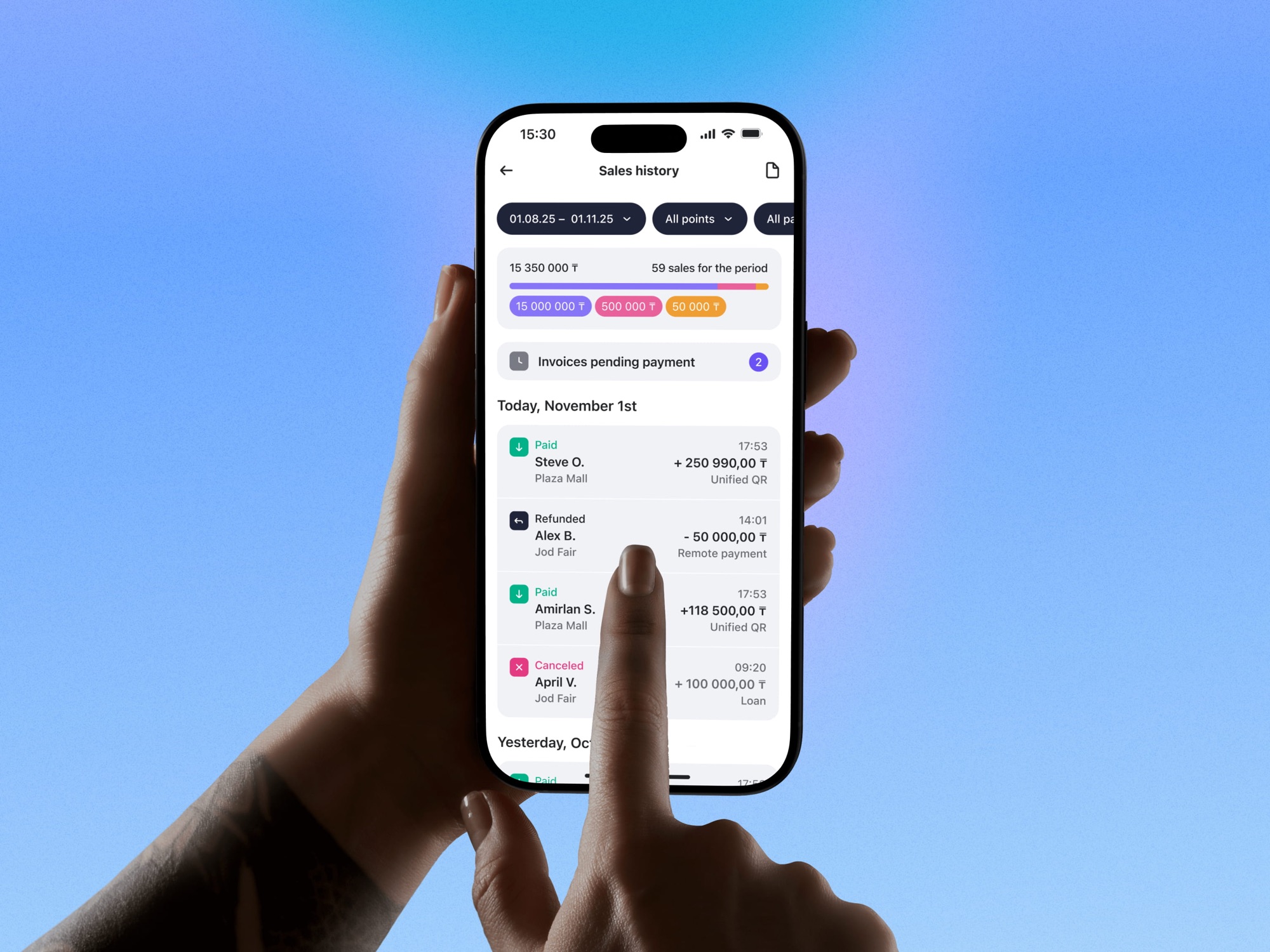

Under that single QR sat three kinds of complexity I had to absorb so the merchant never felt them: interoperability — one code settling across five banks; merchant heterogeneity — sole traders, LLCs, and self-employed each needing a different verification and compliance path (KYB/KYC, limits); and payment states — success, processing, declined, refund, plus multi-POS merchants. I untangled the branching logic with a systems analyst on grooming calls and broke verification into steps, so the hard part stayed inside the system, not on the merchant's screen.

Unified QR flow — the branching reality behind one merchant QR: merchant types, KYB/KYC paths, payment states

Unified QR flow — the branching reality behind one merchant QR: merchant types, KYB/KYC paths, payment states

The Payment Invoice feature needed to ship fast — the full cross-bank version would have taken too long. Shipping a half-built interbank flow to hit the date was the easy path, and the wrong one.

I made a deliberate, team-agreed cut: ship intra-bank first — a complete, coherent flow for clients of the same bank — with an explicit roadmap to extend to interbank, now in active build. Conscious scope debt went back on the roadmap where the team could see it, not buried as a silent compromise.

This is the job in fintech: deciding which complexity the user absorbs and which the roadmap carries — and defending that line in front of a commercial stakeholder or a deadline.

Each feature below ships with a metric attached — because that's how I scoped them at the brief stage.

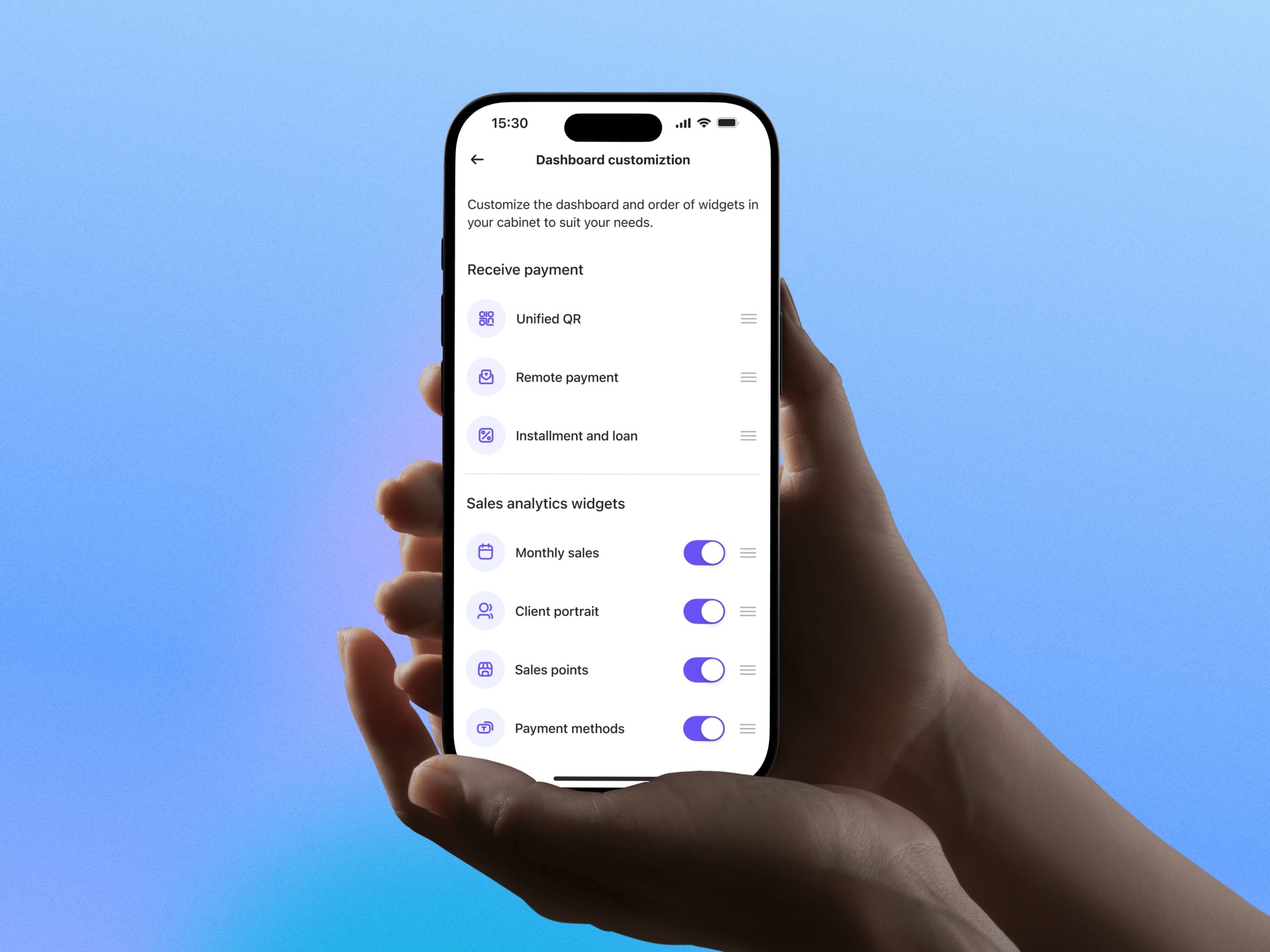

Built the design system from scratch as a parallel track to product features. Goals: consistent UI across iOS, Android, and web admin; predictable handoff for engineering; ability to re-theme without touching components.

92–96% of production colors on tokens, measured by a build-time script in the pipeline — parity is enforced by the system, not asserted on a slide. Reduced handoff time and fewer post-release UI bugs.

This wasn't a side project. The system is the reason new features ship in days instead of weeks, and the reason the product looks coherent across two years of additions.

Components ship with rules, not just pixels. A Button's doc names the pattern (one Primary per view → the main action) and the anti-pattern (never two Primaries → hierarchy collapses; never a Button where a Link belongs → navigation ≠ action; never a colour off-token). That documentation is the context an AI generator needs to produce a real Button, not an invented div.

That governance — documenting the why behind each decision and running design-system workshops with the team — is also how I lead the design function beyond my title: the system holds without me.

Components ship with rules, not pixels — anatomy, states, anti-patterns, and the Token Studio → GitHub pipeline that enforces them

Components ship with rules, not pixels — anatomy, states, anti-patterns, and the Token Studio → GitHub pipeline that enforces them

Governance, not just a library — a documented decision with its why, contribution rules, and the workshop cadence that keeps the system holding without me

Governance, not just a library — a documented decision with its why, contribution rules, and the workshop cadence that keeps the system holding without me

Two years in, Merchant Cabinet is the highest-rated SME banking platform in Kazakhstan.

Merchant Cabinet is more than an SME app. The Unified QR launch lowered the barrier for cashless acceptance in Kazakhstan — a country where SMBs have historically defaulted to cash. The design work here wasn't about pretty screens. It was about deciding what complexity stays inside the system and what reaches the merchant, and getting that line right at country scale.

This case is the proof point that design leadership in B2B fintech is not visual polish or component libraries. It's the discipline of tying every product decision to a hypothesis and a metric — and being willing to defend that line in front of a regulator, a commercial stakeholder, or an engineering lead under deadline pressure.

We were one decision away from shipping an information architecture built on the bank's assumptions. The merchant interviews rewrote it. The lesson I keep relearning: in fintech the hardest design problem usually isn't on the screen — it's the trust underneath it, and you only find it by talking to the people who live in the product.

Concretely, that trust comes down to one thing: making a busy merchant believe the money will arrive, across banks they don't control.

Want to discuss this project?